Aircraft market takes hits

U.S. aircraft production steady (more or less)

General aviation airplane makers in the U.S. posted a steady year, not gaining or losing much ground as a group, but it was a different story in the rest of the world.

It has been a tough year for many airplane makers. As for helicopters, the piston end did well in terms of units sold (an 8.6-percent increase in shipments) but revenue slipped; and the turbine end of the helicopter market may have been tempted toward autorotation by an 8.9-percent decline attributed to tumbling oil prices that tightened belts across the energy sector.

General Aviation Manufacturers Association Chairman Aaron Hilkemann breezed through the not-so-rosy and still incomplete numbers in about five minutes, noting that the turbine helicopter decline was “related to the oil and gas segment, where a lot of those shipments have gone.”

There are asterisks in GAMA’s report, since Finmeccanica Helicopters has not yet provided fourth-quarter data. The same is true of beleaguered Bombardier, Inc., the business jet market leader in 2012 that has since fallen on hard times.

The Canadian firm has had a tumultuous couple of years of well-documented struggles, with airline customers fleeing from the C Series commuter jet to which Bombardier tied much of its future. The company has spent a pile of cash on developing the new airliner and not taken a firm order for it since 2014. The Canadian press reports that the company now hopes to sell turboprop airliners to stay afloat while the search for C Series customers continues. Bombardier is expected to report its 2015 financial data Feb. 17, and investors do not expect that to be pretty.

Hilkemann said GAMA would update its overall numbers when Bombardier provides its business jet sales data, which the organization plans to release Feb. 18. That data will significantly impact GAMA’s reported totals and year-over-year percentage calculations for the jet and overall GA market, since the company, while trailing Gulfstream Aerospace Corp., still held 28 percent of the world business jet market in 2014. (GAMA excluded Bombardier sales for both years to make the 2015 comparisons announced Feb. 10.)

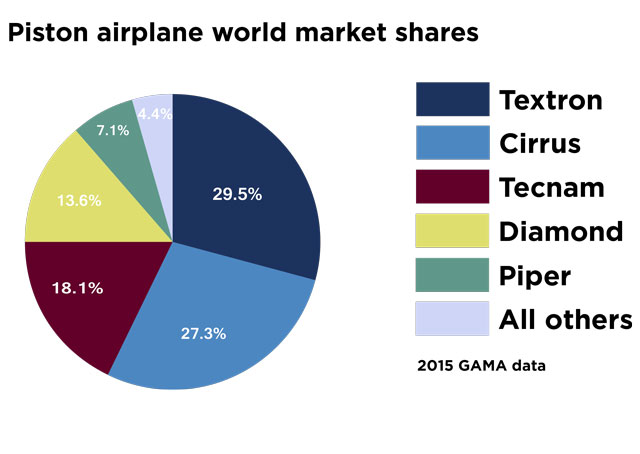

All participating manufacturers provided piston data in time for the Feb. 10 release. That part of the report showed continued piston market dominance by a handful of U.S. airplane makers, with Textron Aviation passing Cirrus Aircraft for the overall lead.

While piston airplane shipments slipped 6.5 percent worldwide, U.S. piston airplane shipments declined less than 1 percent. Cirrus posted a slight decline in airplanes sold (down to 301 from 308), but increased billing slightly to $221 million. Textron, owner of the Cessna and Beechcraft brands, pushed past Cirrus (taken as a whole) with 312 piston airplanes sold between those brands.

Piper Aircraft piston sales slid nearly 14 percent, leaving it fifth in world piston airplane production, trailing foreign makers Diamond Aircraft Industries, Inc. and Tecnam, which showed strength in a declining market by selling one more airplane (for a total of 191) and boosting revenue by 18 percent, which also happens to be Tecnam’s share of the world piston market. Next on that list is Diamond Aircraft Industries, Inc., which posted declines of nearly 30 percent in sales and billing for 2015, leaving it with just under 14 percent of the piston market.

In 2014, Piper and Flight Design, the German maker of light sport aircraft, each shipped 88 piston airplanes (Piper’s overall total was 172 aircraft shipped). In 2015, Piper’s piston shipments declined to 75, while Flight Design, which suffered the effects of fighting in Ukraine disrupting supply lines and delaying deliveries, saw deliveries drop to 59, down by a third, along with revenue. (Flight Design USA, the distributor for North America, recently announced a deal to produce aircraft for the U.S. market in Taiwan, in addition to the factory in Ukraine.

Cirrus, Textron, and Piper together account for two-thirds of world piston airplane production, and 87 percent of U.S. piston airplane production (though sales data for Aviat Aircraft has not been included in GAMA reports issued to date, so those numbers might bear slight adjustment).

Turboprop sales slumped just about everywhere, down 10.3 percent among U.S. airplane makers and down 7.3 percent worldwide. (GAMA reported a 7.6-percent worldwide decline, but there appears to be an arithmetic error in GAMA’s 2014 turboprop count that boosted 2014 total sales by two airplanes, accounting for the slightly different percentage decline).

Air Tractor and Thrush Aircraft, makers of turboprop airplanes for agriculture, continued to see double-digit percentage declines in units sold in 2015, enough to account for much of the overall (and ongoing) softness of the sector. (Each company managed a slight increase in revenue despite shipping fewer airplanes.)

In the larger turboprop segment, high-end sales slipped more than the lower end, explaining the 10.8-percent decline in turboprop market value to $1.65 billion, Hilkemann said.

GAMA President Pete Bunce directed most of his state-of-the-industry remarks at the FAA reauthorization bill a week after it first landed in Congress. The bill, and more so the law that will eventually come of it, stands to affect GA in many significant ways. Bunce said that the bill contains many elements manufacturers welcome, including “strong language” to reform and streamline the aircraft certification process.

“This is our lifeblood,” Bunce said. “We are wasting too much time and effort, as well as the regulatory authorities, to have engineers checking engineers.”

That phrase, “engineers checking engineers,” was repeated in reference to ongoing international efforts to increase reciprocity in matters of certification, maintenance, and aircraft modifications.

Bunce praised congressional efforts toward pilot medical certification reform: “There’s some really good language in this bill that we as manufacturers, as well as our sister associations, feel very passionate about,” Bunce said.

Bunce said proposed user fees for charter and airline operators were problematic, but that the process of making the new law had only just begun. He also said the proposal to split air traffic control from the rest of the FAA would require the creation of a new bureaucracy within the U.S. Department of Transportation to manage the new ATC manager, since few DOT employees (other than those who work for the FAA) know the intricacies of the National Airspace System.

“Suffice to say, just in the House, there are many quarters to play in this game before we get over to the Senate,” Bunce said.

Jim Moore

Related Articles