GA a force in national, local economies

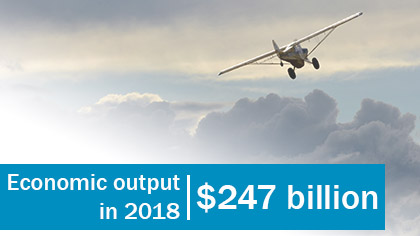

General aviation is a $247 billion industry that employed 273,500 workers and indirectly supported 1.2 million jobs while keeping a fleet of more than 211,000 aircraft flying for business and individual operators in 2018, according to a new report that analyzed the industry’s impact and output.

The report, Contribution of General Aviation to the US Economy in 2018, found an upbeat trend in key metrics since the last industry update from 2013. The document, released February 19, was prepared for seven industry associations, including AOPA, by consulting firm PricewaterhouseCoopers.

Other industry-association leaders used words like “dynamic” and “powerhouse” to describe GA’s vital signs in comments to their memberships.

You can measure GA’s importance to the economy from various vantage points—and the report covered the bases, noting that each of the 273,500 full- and part-time jobs directly involved in GA “supported 3.3 jobs elsewhere in the economy.”

Also, it said, the industry generated $77 billion in labor income—that’s wages, salaries, benefits, and proprietors’ income—and kicked in $128 billion to U.S. gross domestic product. (GDP is the value of the goods and services produced in the United States. GDP was $20.49 trillion in 2018.)

You know the old saying: A billion here and a billion there, and pretty soon you’re talking real money. In light of that adage, here’s a way to bring lofty GDP data down to earth: “Overall, total GDP impact attributable to general aviation amounted to approximately $393 per person in the United States in 2018,” the report said.

Who were the GA players, and what did they do to turn in the results quantified in the report’s 58 pages of data, charts, and breakouts?

PricewaterhouseCoopers defined the scope of GA as “the manufacture and operation of any type of aircraft that has been issued an airworthiness certificate by the FAA, other than aircraft used for scheduled commercial air service or operated by the military.”

It defined the fleet as “personal-use aircraft, business aircraft, helicopters, aircraft operated by flight schools, and on-demand passenger or cargo transportation under Federal Aviation Regulation Part 135.”

Some selected highlights of the report:

- In 2018, the fleet logged 25.5 million flight hours in the United States. Single-engine piston airplanes flew 47 percent of those flight hours, with jets accounting for 18 percent, and helicopters, 11.5 percent.

- The majority of the active GA fleet, at 61 percent, consisted of piston singles. Experimentals, including special light sport aircraft, added a 13-percent share. Jets accounted for 6.9 percent; piston twins, 6 percent; and turboprops, 4.6 percent.

- Approximately 2,970 U.S.-manufactured and experimental amateur built GA aircraft were delivered in 2018, with piston-powered aircraft accounting for 28 percent of all shipments, followed by experimental aircraft (769 aircraft, or about 26 percent), jets (15.9 percent), and turboprops (14.9 percent), it said.

- Citing FAA figures, the report identified the kinds of flight hours GA pilots flew in 2018. “For general aviation, most of the flight hours (nearly 80 percent) fall into three use types: (1) personal, (2) business (with or without a paid crew), and (3) instructional. Other uses of general aviation aircraft include agricultural and forestry applications, aerial observation and sight-seeing, non-Part 135 air medical services, and other work uses. On-demand Part 135 uses include air taxis, air tours, and air medical services,” it said.

- GA’s economic reach touched all 50 states and Washington, D.C. The top 10 states (as ranked by jobs attributable to GA) provided 53 percent of industry jobs.

AOPA, the General Aviation Manufacturers Association, the Aircraft Electronics Association, the Experimental Aircraft Association, Helicopter Association International, the National Air Transportation Association, and the National Business Aviation Association sponsored the report, with support from Jetnet LLC and Conklin & de Decker.